The Tax Administration Laws Amendment Act, 2026 (Act No. 4 of 2026), assented to by the President of South Africa on 31 March 2026 and published in Government Gazette No. 54447 dated 1 April 2026, introduces several significant changes to the TaxAdministration Act, No. 28 of 2011 (“TAA”), including amendments affecting understatement penalties.

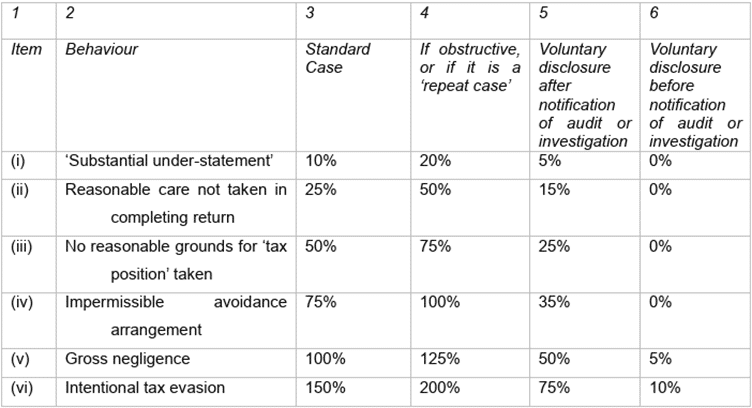

Among the most relevant for taxpayers are revised provisions dealing with Suspensions of Payment and the Remission of Understatement Penalties, per the “Understatement penalty percentage table” as contained in section 223 of the TAA:

Suspensions of Payment – “Just a Breather”

With the 2026 filing season looming in the near future, taxpayers must be mindful that should they fail to file their income tax returns, or timeously provide relevant information, the South African Revenue Service (SARS) will issue an estimated assessment, under which the purported debt is immediately due and payable.

Noting SARS’ far-reaching collection powers, it can in such cases, move swiftly to attach taxpayers’ bank accounts, garnish salaries, and attach assets, all before the taxpayer has had a chance to prove that the estimated assessment is excessive or even incorrect.

A measure of relief is offered to taxpayers with the amendment to section 164 of the TAA, now expressly encompassing that a taxpayer who requests, or intends to request, a reduced assessment under section 95(6) of the TAA, may apply for a Suspension of Payment.

On paper, this means that while SARS considers whether to issue a reduced assessment, the taxpayer may secure temporary relief from the immediate threat of enforced collection by SARS.

Ring-fencing “Bona Fide Inadvertent Error” – an Incomplete Defence

Section 222(1) of the TAA has historically forgiven innocent mistakes, by providing taxpayers reprieve in that no understatement penalty is payable if the understatement results from a bona fide inadvertent error.

Although cased broadly, this was not the practical application, and the legislative amendments to sections 222 and 223, do not remove this saving grace. Rather, it clarifies that the carve-out was only ever meant to apply to cases of substantial understatement (penalty of 20% or less), being a category triggered by an objective calculation, not by taxpayer behaviour (up to 200%).

- Section 222(1) Amendment: For tax understatements involving behaviour subject to a penalty per section 223, the taxpayer is required to pay the understatement penalty in addition to the tax due, removing the exception for bona fide inadvertent errors as a standalone relief.

- Section 223(3) Substitution: SARS must grant remission for penalties imposed for substantial understatements if either: (a) The understatement arose from a bona fide inadvertent error; or (b) The taxpayer made full disclosure of the arrangement causing prejudice to SARS/fiscus by the return due date and held a favourable independent opinion by a registered tax practitioner issued by no later than the return due date, confirming the likely legal standing of the taxpayer’s position.

This amendment emphasises full disclosure and professional tax advice as critical factors in penalty remission eligibility.

Other Noteworthy Amendments to the TAA

- Legal Proceedings Notification (Section 11): A minimum 10 business days’ written notice to SARS is required before instituting legal proceedings in the High Court, unless otherwise directed by the court.

- SARS Official Premises Inspection (Section 45): SARS officials may conduct inspections without prior notice at premises suspected of carrying on a trade or enterprise to verify: – The occupier’s identity and registration for tax. – The existence and suitability of the physical address provided in registration applications for conducting stated activities. – Compliance with sections 29 and 30 (registration and tax obligations).

- Protection of Sensitive Information (Section 68): Disclosure of information likely to prejudice the economic interests or financial welfare of South Africa, including contemplated changes to taxes, levies, duties, penalties, or interest, is restricted.

- Clarifying Non-applicability of Underpayment Definitions (Section 227): The amendments clarify that certain penalties and definitions in the Tax Administration Act do not apply to underpayments as defined in the Customs and Excise Act.

- Service of Notices to Companies (Sections 247 and 249): SARS may serve notices at addresses provided by companies under specified sections, and companies are required to maintain a continuously filled office for receiving such notices.

The Tax Administration Laws Amendment Act, 2026 introduces important clarifications and procedural enhancements to the administration of tax disputes, penalty relief, and enforcement actions by SARS.

Key changes enable taxpayers to seek payment suspension under more defined conditions while ensuring SARS can exercise discretion to protect fiscal interests. The amendments on understatement penalties prioritise disclosure and professional tax opinions, fostering transparency and compliance.

Should you already find yourself on the wrong side of SARS, there is a first mover advantage in seeking the appropriate legal counsel, ensuring the necessary steps are taken, under legal professional privilege, and providing a degree of protection. In instances of “risk”, SARS must be engaged legally, and we generally find them utmost agreeable where a correct tax and compliance strategy is followed.